Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Off-balance sheet financing is an accounting practice used to keep certain assets or liabilities from appearing on a company’s balance sheet. Companies use off-balance sheet financing to maintain lower leverage ratios, comply with debt covenants, and manage financial risk while preserving access to funding and liquidity.

Off-balance sheet financing requires transparent disclosure in the financial statement notes so investors can assess the company’s true financial exposure. When structured responsibly, off-balance sheet financing supports capital efficiency and long-term growth.

However, when off-balance sheet financing is used to obscure risk or hide liabilities, the accounting practice can mislead investors and damage financial credibility.

Common methods of off-balance sheet items include lease commitments, special-purpose vehicles, factoring arrangements, joint ventures, and sale-and-leaseback transactions. These structures help companies fund operations, isolate financial risk, or maintain access to assets without recording new liabilities on the balance sheet.

Each of these methods achieves the same underlying goal: separating financial obligations from the company’s balance sheet while retaining access to assets or funding.

Companies must disclose off-balance sheet arrangements in the notes to their financial statements under both US GAAP and IFRS accounting standards. These disclosure requirements ensure that investors and creditors can assess the company’s true financial exposure, even when certain obligations don’t appear directly on the balance sheet.

The US Securities and Exchange Commission (SEC) also requires disclosure of material off-balance sheet financing in financial statement footnotes, including potential impact on liquidity, capital resources, and operational results.

When companies fail to provide adequate disclosure, they risk regulatory penalties, loss of investor confidence, and potential legal liability.

Off-balance sheet financing appeals to companies because it can strengthen key financial metrics while maintaining operational flexibility. By keeping certain liabilities or assets off the balance sheet, a company may appear less leveraged, improving investor confidence and access to credit.

The practice can also help a business preserve borrowing capacity. When debt ratios remain low, lenders view the company as a lower credit risk, which can result in better loan terms or higher borrowing limits. At the same time, transactions like leasing or receivable factoring can provide immediate liquidity without adding new debt.

There are also tax and accounting advantages. In some cases, payments related to off-balance sheet arrangements are treated as operating expenses rather than capital expenditures, which can reduce reported taxable income.

When structured properly, off-balance sheet financing provides a practical way for companies to manage liquidity and capital efficiency while maintaining compliance with debt covenants and disclosure standards.

Off-balance sheet financing can introduce serious risk if it’s used to disguise debt or mislead investors. When companies rely too heavily on these arrangements, they risk creating hidden obligations that undermine transparency and investor trust.

The Enron scandal remains the most cited example, where off-balance sheet entities concealed billions in debt and failing investments. The company’s collapse led to stricter global reporting standards and tighter oversight of off-balance sheet arrangements.

Ultimately, the same flexibility that makes off-balance sheet financing appealing can also make it dangerous if used without transparency and oversight.

Off-balance sheet financing keeps certain liabilities off the balance sheet to improve financial ratios, but it requires transparent disclosure to avoid misleading investors.

The key for investors and analysts is understanding that healthy-looking leverage ratios may not tell the complete story. Always review footnote disclosures about special-purpose entities, joint ventures, and contingent obligations to assess a company’s true financial exposure and hidden commitments.

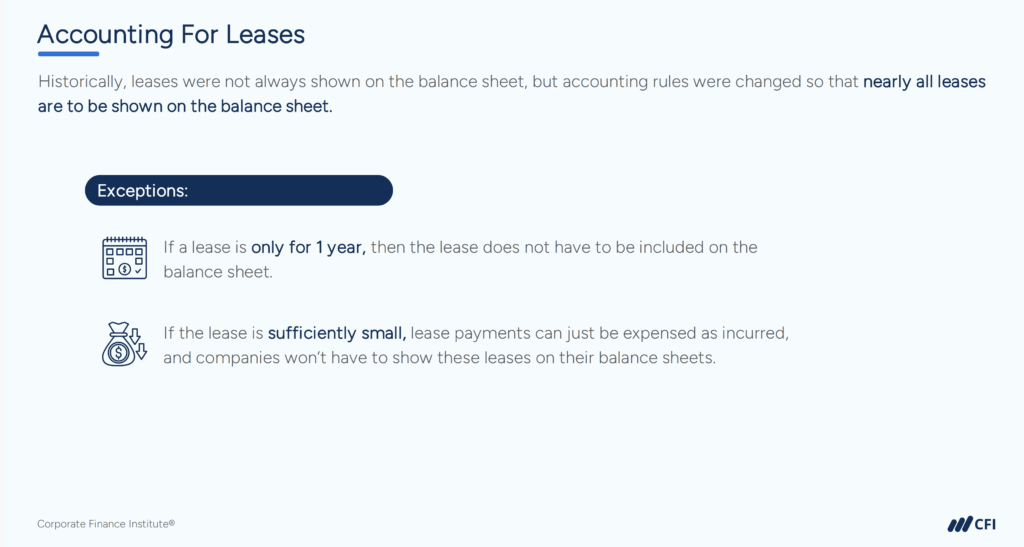

A common example is an operating lease, where a company rents an asset for long-term use. Before recent accounting changes, the lease obligation didn’t appear on the balance sheet, only the expense did.

Companies use off-balance sheet financing to improve financial ratios, preserve borrowing capacity, or manage risk without adding reported debt. Off-balance sheet financing is legitimate if structured transparently and disclosed properly.

Yes. Off-balance sheet financing is legal when it complies with accounting standards and is disclosed properly. Problems occur only when companies use it to hide liabilities or mislead investors.