Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The trade lifecycle is the end-to-end process for buying or selling securities in financial markets. The trade lifecycle includes initiation, order matching, trade capture, confirmation, custodian instructions, clearing, and settlement.

The lifecycle of a trade demonstrates how capital markets move securities and cash between buyers and sellers through a coordinated market infrastructure. Finance professionals handle different trade lifecycle stages depending on their role.

For example, traders execute orders through exchanges or OTC markets. Middle-office teams confirm trade details and manage risk exposure, and back-office operations ensure custodians receive accurate settlement instructions.

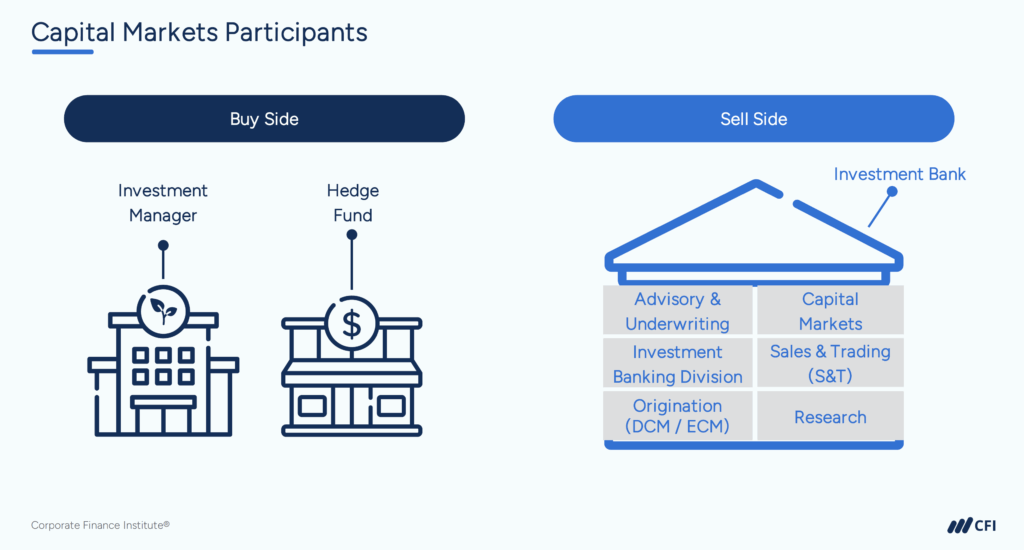

Trade initiation is the first stage of the trade lifecycle and begins when a buy-side investor decides to buy or sell a financial instrument, such as a stock or bond. Fund managers make investment decisions based on research analysis and relay these decisions to traders for execution.

Research analysts evaluate securities and form opinions. Buy-side analysts conduct research for internal use, while sell-side analysts provide reports to buy-side clients. Buy-side fund managers rely on this research to decide on trades. Once a decision is made, buy-side traders instruct sell-side sales traders, who then pass orders to sell-side traders for execution.

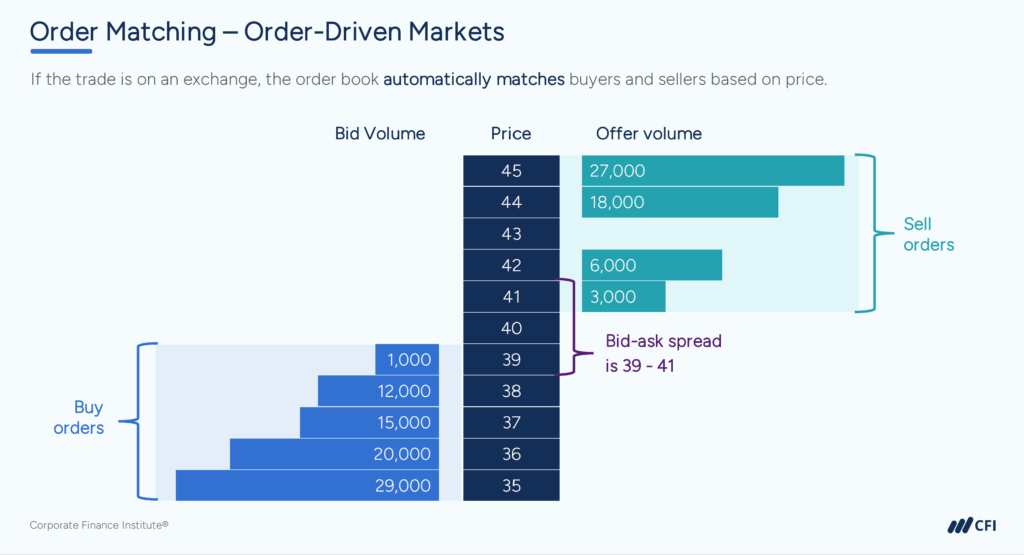

Order matching is the stage where a seller is found for a buyer or vice versa. Once a sell-side trader receives an order, the trade is recorded in the order management system and matching begins.

Order matching occurs in exchange-traded markets or over-the-counter (OTC) markets.

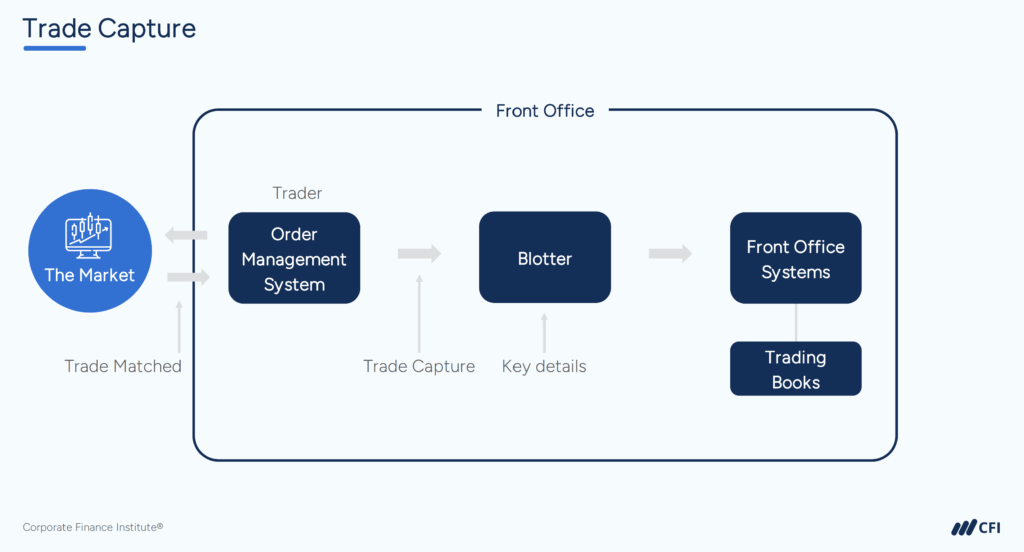

Trade capture is when critical trade details are entered into front office systems after a trade is matched and executed. Trade details transition from the trader’s order management system to a trade blotter.

A trade blotter is a real-time log monitoring executed trade details including date, time, instrument, quantity, price, and counterparty information. These details feed into other critical systems throughout the financial institution.

Trading books maintain a record of each executed trade for gain and loss calculations. At the end of each day, positions are valued through marking to market. Realized gains or losses are calculated for closed trades, and unrealized gains or losses are calculated for open trades based on closing prices.

Product control, a middle-office team, obtains prices using multiple data sources to ensure accuracy.

Risk management systems capture trade details to monitor counterparty risk, market risk, and credit risk. Compliance systems ensure trades comply with regulatory requirements and internal policies for regulatory reporting, surveillance, and audit purposes.

If front office systems flag issues, those must be resolved. If no issues are found, the trade is authorized and ready for the next stage.

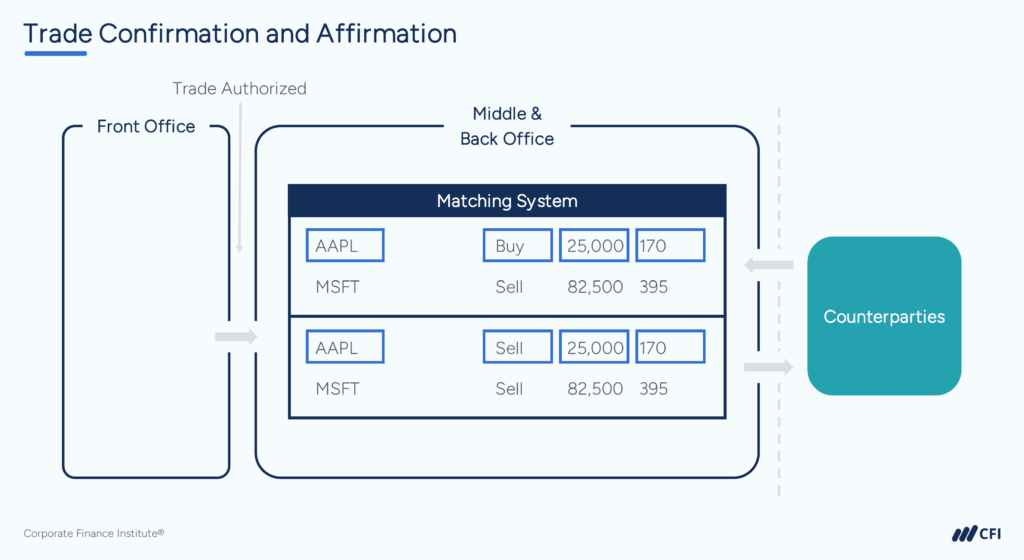

Trade confirmation and affirmation occur very soon after trade capture when counterparties check and affirm that the trade details are correct. Once authorized by front-office systems, trade details enter a matching system awaiting counterparty details. Each counterparty shares their trade record (trade confirmation), and the matching engine compares records.

A matching engine compares the security (using identifiers), buy/sell direction, volume, and price. If details align, both parties electronically affirm the trade.

If discrepancies arise, the trade is flagged as unmatched and requires investigation involving counterparty communication and possibly original traders. A failed resolution may result in trade cancellation, damaging relationships, and exposing the institution to market risk.

Trade enrichment is the process of adding trade details called Standard Settlement Instructions (SSIs). SSIs provide additional information that ensures the buyer’s custodian bank receives the correct securities and the seller’s custodian bank receives the correct payment.

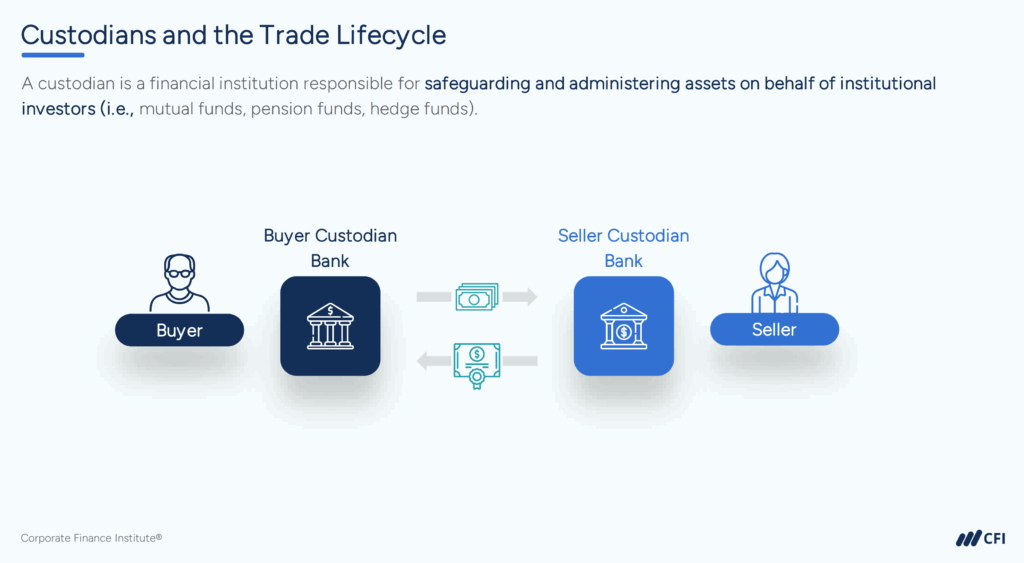

Custodian banks are financial institutions that safeguard assets for buy-side institutional investors. In the trade lifecycle, custodians facilitate settlement by transferring securities and funds between trading counterparties. The buyer’s custodian transfers cash and receives securities, while the seller’s custodian transfers securities and receives cash.

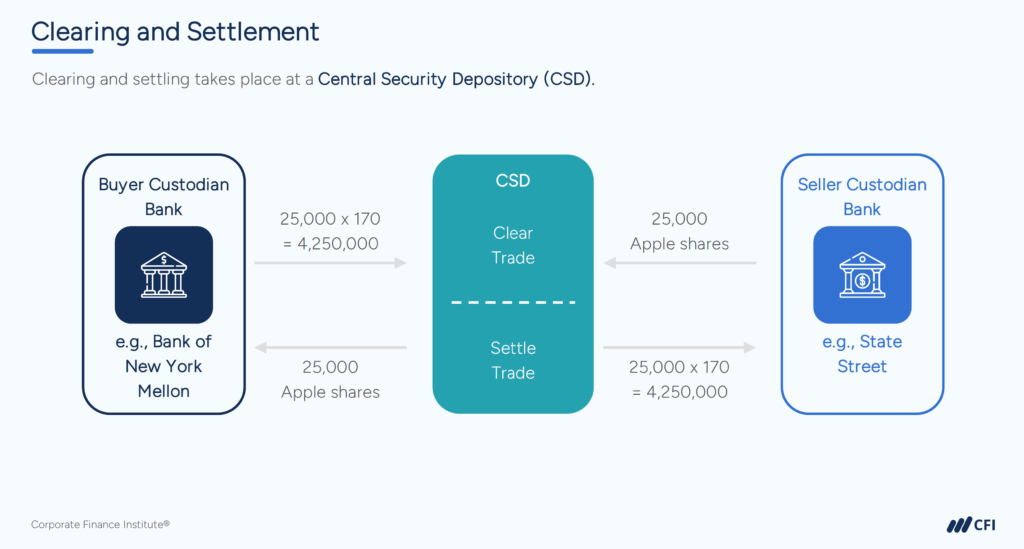

Clearing and settlement is the final stage where securities and cash are exchanged and legal ownership transfers from seller to buyer. This stage resolves a critical issue: neither custodian is comfortable transferring assets until receiving the counterparty’s assets.

A Central Securities Depository (CSD) acts as an intermediary between custodian banks, which maintain accounts with the CSD for that market. The CSD has two main jobs:

The Depository Trust and Clearing Corporation (DTCC) is the US national CSD. Other countries have their own national CSDs, such as Euroclear UK and Ireland.

Most capital market trades now settle in two days (T+2), down from the traditional five days (T+5). Bonds can take one to three days, while some markets like China settle on the same day (T+0).

The trade lifecycle is a sequence of steps that move a security transaction from initial buy or sell decision through final settlement. This process includes trade initiation, order matching, trade capture, trade confirmation and affirmation, trade enrichment, instructing custodians, and clearing and settlement.

The trade lifecycle consists of trade initiation, order matching, trade capture, trade confirmation and affirmation, trade enrichment, instructing custodians, and clearing and settlement.

The trade lifecycle typically takes two business days (T+2) from trade execution to final settlement for most capital market securities.

Clearing is when the Central Securities Depository (CSD) verifies that custodians sent the correct securities and cash. Settlement is when money and securities actually move between custodian banks and legal ownership transfers from seller to buyer.

Custodian banks are financial institutions that safeguard assets for buy-side institutional investors. In the trade lifecycle, custodians facilitate settlement by transferring securities and funds between trading counterparties.

Ready to go deeper? CFI’s Lifecycle of a Trade course teaches you to identify all participants, execute trades across different market mechanisms, and manage confirmation, clearing, and settlement processes. This course is a requirement for CMSA® Certification, CFI’s program focused on preparing you for capital markets roles.

Explore Lifecycle of a Trade ➡️